How To Get A Line Of Credit On My House

What is a home equity line of credit?

A home equity line of credit, or HELOC, is a second mortgage that gives you access to cash based on the value of your home. You can draw from a home equity line of credit and repay all or some of it monthly, somewhat like a credit card.

With a HELOC, you borrow against your equity, which is the home's value minus the amount you owe on the primary mortgage. You can also get a HELOC if you own your home outright, in which case the HELOC is the primary mortgage rather than a second one.

NerdWallet Guide to COVID-19

Get answers to questions about your mortgage, travel, finances — and maintaining your peace of mind.

How does a home equity line of credit work?

Much like a credit card that allows you to borrow against your spending limit as often as needed, a HELOC gives you the flexibility to borrow against your home equity, repay and repeat.

Most HELOCs have adjustable interest rates. This means that as baseline interest rates go up or down, the interest rate on your HELOC will adjust, too.

To set your rate, the lender will start with an index rate, then add a markup depending on your credit profile. Generally, the higher your credit score, the lower the markup. That markup is called the margin, and you should ask to see the amount before you sign off on the HELOC.

How do you qualify for a home equity line of credit?

Lender requirements will vary, but here's what you'll generally need to get a HELOC:

-

A home value that's at least 15% more than you owe.

Put your home equity to work

Know what you have to borrow by tracking your home's value and mortgage balance together.

How to get a home equity line of credit

The process of getting a HELOC is similar to that of a purchase or refinance mortgage. You'll provide some of the same documentation and demonstrate that you're creditworthy. Here are the steps you'll follow:

-

Once you have pulled together your documentation and selected a lender, apply for the HELOC.

-

You'll receive disclosure documents . Read them carefully and ask the lender questions. Make sure the HELOC will fit your needs. For example, does it require you to borrow thousands of dollars upfront (often called an initial draw)? Do you have to open a separate bank account to get the best rate on the HELOC?

-

The underwriting process can take hours to weeks, and may involve getting an appraisal to confirm the home's value.

-

The final step is the loan closing, when you sign paperwork and the line of credit becomes available.

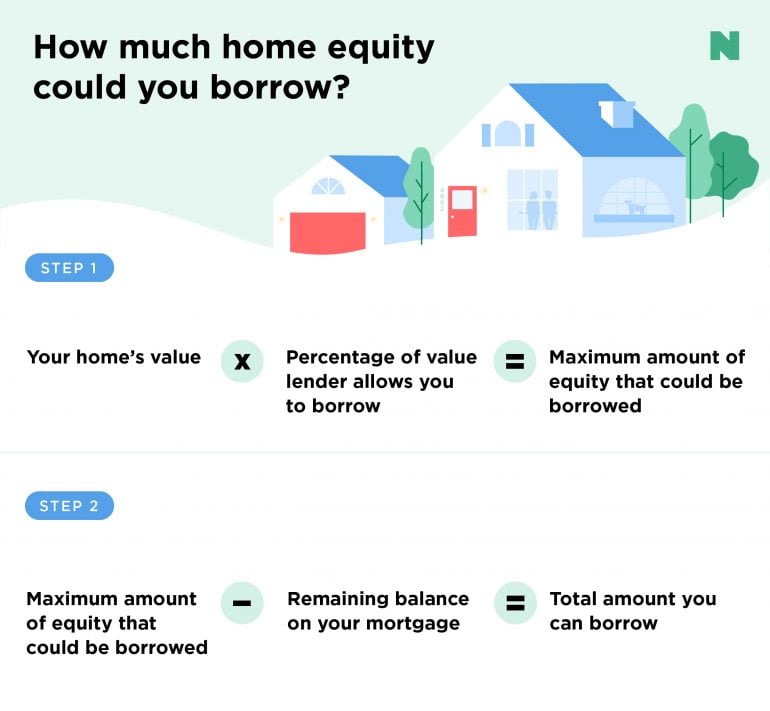

How much can you borrow with a HELOC?

The maximum amount of your home equity line of credit will vary based on the value of your home, what percentage of that value the lender will allow you to borrow against and how much you still owe on your mortgage. Two quick calculations can give you an idea of what you might be able to borrow with a HELOC.

Say you have a $500,000 home with a balance of $300,000 on your first mortgage and your lender will allow you to access up to 85% of your home's value. Multiplying the home's value ($500,000) by the percentage the lender will allow you to borrow (85%, or .85) gives you a maximum amount of $425,000 in equity that could be borrowed. Subtract the amount you still owe on your mortgage ($300,000) to get the total amount you can borrow with a HELOC — $125,000.

Or skip doing the math, and use the HELOC calculator below to see how much you might be able to borrow.

How do you pay back a home equity line of credit?

A HELOC has two phases: the draw period and the repayment period.

During the draw period , you can borrow from the credit line by check, transfer or a credit card linked to the account. Monthly minimum payments often are interest-only during the draw period, but you can pay principal if you wish. The length of the draw period varies; it's often 10 years.

During the repayment period , you can no longer borrow against the credit line. Instead, you pay it back in monthly installments that include principal and interest. With the addition of principal, the monthly payments can rise sharply compared with the draw period. The length of the repayment period varies; it's often 20 years.

At the end of the loan, you could owe a large lump sum — or balloon payment — that covers any principal not paid during the life of the loan. Before you close on a HELOC, consider negotiating a term extension or refinance option so that you're covered if you can't afford the lump sum payment.

Nerdy tip: If you plan to move any time soon, a HELOC may not be the right choice for you. When you sell your home, you'll have to pay off the balance of the HELOC (after all, you can't borrow the equity of a home you don't own). Paying off the home equity line of credit could cut into any profits you might be making from your home's sale. You may also have to pay a cancellation fee to the lender.

Is getting a HELOC a good idea?

Whether a home equity line of credit is a good idea really comes down to your goals and financial situation. A HELOC is often used for home repairs and renovations, which can increase your home's value. Another bonus: The interest on your HELOC may be tax-deductible if you use the money to buy, build or substantially improve your home, according to the IRS.

Some use home equity lines of credit to pay for education, but you may get better rates using federal student loans . Financial advisors generally don't recommend using a HELOC to pay for vacations and cars because those expenditures don't build wealth, and may put you at risk of losing the home if you default on the loan.

What are the disadvantages of a home equity line of credit?

The main drawback of a HELOC is that it increases the risk of foreclosure if you can't pay the loan. Regardless of your goal, avoid a HELOC if:

Your income is unstable. If it's possible that your income will change for the worse, a HELOC may be a bad idea. If you can't keep up with your monthly payments, your lender could force you out of your home.

You can't afford the upfront costs . A HELOC may require an application fee, title search, home appraisal , attorney's fees and points. These charges can set you back hundreds of dollars.

" The upfront costs of a HELOC may not be worth it if you need only a small line of credit. "

You aren't looking to borrow much money. A HELOC's upfront costs may not be worth it if you need only a small line of credit. In that case, you may be better off with a low-interest credit card , perhaps with an introductory interest-free period.

You can't afford an interest rate increase. HELOCs have adjustable rates. The loan paperwork will disclose the lifetime cap, which is the highest possible rate. Could you afford a monthly payment with that much interest? If not, think twice about getting the loan.

You're using it for basic needs. If you need extra money for day-to-day purchases, and you're having trouble just making ends meet, a HELOC isn't worth the risk. Get your finances in shape before taking on additional debts.

Variable rates leave you vulnerable to rising interest rates. Be sure to take this into account. Look at the size of the periodic cap (that's how much the interest rate can change at any one time) and the lifetime cap (the highest interest rate you could be charged over the life of the loan) to get an idea of how high your payments could get.

On the plus side, as with a credit card, you only pay interest on the amount of money you use, not the total amount available to borrow.

Getting the best HELOC rate

This one's on you: The more you research, the bigger your reward. As you look for the best HELOC rates, get quotes from various lenders. Check your primary bank or mortgage provider; it might offer discounts to existing customers. Get a quote and compare its rates with at least two other lenders. As you shop around, take note of introductory offers like initial rates that will expire at the end of a given term.

How a HELOC affects your credit score

Although a HELOC acts a lot like a credit card, giving you ongoing access to your home's equity, there's one big difference when it comes to your credit score : Some bureaus treat HELOCs of a certain size like installment loans rather than revolving lines of credit.

This means borrowing 100% of your HELOC limit may not have the same negative effect as maxing out your credit card. Like any line of credit, a new HELOC on your report will likely reduce your credit score temporarily. However, if you borrow responsibly — making timely payments and not utilizing the full credit line — your HELOC could help you improve your credit score over time.

Is it better to get a home equity loan or line of credit?

That depends on your financial situation and needs. A HELOC behaves like a revolving line of credit, letting you tap your home's value in the amount you need as you need it. A home equity loan works more like a conventional loan, with a lump-sum withdrawal that's paid back in installments.

HELOCs typically have variable interest rates, while home equity loans are usually issued with a fixed interest rate. This can save you from a future payment shock if interest rates rise. Work with your lender to decide which option is best for your financing needs.

How To Get A Line Of Credit On My House

Source: https://www.nerdwallet.com/article/mortgages/heloc-home-equity-line-of-credit

Posted by: campbellcaming.blogspot.com

0 Response to "How To Get A Line Of Credit On My House"

Post a Comment